Introduction

The growth of Sea-Tac Airport has definitely not been linear. There have been many fits and starts that don’t make for easy sound bites. For example, Sea-Tac Airport was able to run over 400,000 operations in 2000 on only two runways.

By the time the Third Runway opened for business on November, 20 2008, new technology was becoming available which would have negated any immediate need for its construction! In hindsight, one wonders what the Port got for that $1.1 billion dollar cost.

Here is a timeline of key events that contributed to the airport’s ability to grow its operations and increase its cash flow.

1996 PSRC go ahead

After performing the required demand study, the Puget Sound Regional Council approves the Port of Seattle’s plan to build a Third Runway.

As one condition for this permission, the Port identifies 11,000 homes within a geographic boundary referred to as the DNL65. The Port agrees to fit these homes with sound insulation systems, referred to as ‘Port Packages’. Roughly 9,400 are completed before the Third Runway opens in 2008.

1997 EIS

The City of SeaTac comes to an agreement with PoS for $10MM to build new City Hall, drops out of opposition.

A full Environment Impact Statement (EIS) is published with detailed predictions on the effects to surrounding communities and suggested mitigations totaling almost $1 billion ($289 million for Des Moines alone.) None of those recommendations are ever acted upon.

In private, the ACC concedes the cause is probably lost.

1998 Wetlands?

Delta Airlines questions economics of third-runway plan. Port discovers wetlands on the dedicated SR-509 exit for fill dirt trucks. , Withdraws plan in order to rewrite it. When asked why fill dirt was being delivered before permit approval, Port spokesman Bob Parker says, “I’m told by people who know that you can’t wait for all your permits to begin work. If you did, you’d never get anything done.”

In private, ACC members share renewed optimism.

1999 Revised Plan

Port submits revised third-runway plan; community opponents attack it on technical, environmental, and economic grounds. Former Port Environmental Manager Barbara Hinkle resigns and joins anti-Third Runway movement.

2000 Costs

Finish date for third runway slips to 2006, cost estimate rises to $770 million (from original $330 million.) Total cost of airport improvement through 2009 now set at $3.4 billion (from original $1.1 billion.)

2001

The tragedy of 9/11 2001 was transformative for all airports. Air traffic slowed dramatically for a short time, but was also slow to recover. In purely logistical terms it made it tougher to process passengers and cargo.

2003 Water Quality

After a series of lawsuits usng data collected by Regional Commission on Airport Affairs (RCAA) consultant Greg Wingard, the Port finally complete its first sewer and stormwater systems. This saves all major creeks in the area (Massey, Miller, Barnes, Des Moines, McSorley) from fiftyyears of environmental damage where airfield run off was going directly into Puget Sound..

The downside? Approval of the final Army Corp of Engineers and State permits removes the last roadblock to construction of the Third Runway.

2004 Construction begins

After thirteen years and $15.5MM, the Airport Communities Coalition (ACC) finally exhausts all legal options and packs it in. The settlement includes a cost sharing agreement to provide $150 million sound insulation for Highline Schools.

2007 – The Shift

As soon as construction on the Third Runway begins, General Aviation and Air Taxis drop off. The Port (with the full support of the FAA) decided to push those flights north to KCIA and Boeing Field, which are better suited to GA.

Part of this move was practicality. Carriers such as Southwest were making serious plans to move to Boeing Field. That loss in revenue would have blown a giant hole in the re-payment strategy for the Third Runway. the Port had to prioritize carriers over GA. The other consideration was strategic. By making Sea-Tac a carrier-only airport, the revenue opportunities became much greater.

There’s capacity and then there’s capacity…

In 2000, there’s almost a 50/50 mix of Air Carrier (737, 747, 777, etc.) and Air Taxis.

| Year | Air Carrier Operation | Air Taxi Operation | General Aviation Operation | Military Operation | Total Operations |

| 2000 | 236,355 | 203,723 | 5,448 | 95 | 445,621 |

Here is 2019, the first time the airport surpassed those 2000 numbers. Now small planes make up less than two 2% of the mix, replaced almost entirely by commercial jets.

| 2019 | 443,817 | 4,456 | 2,135 | 79 | 450,487 |

+2008

Third Runway construction is completed and the first test flights occur in August. The community groups CASE and RCAA pack it in almost to the day, dumping literally years of valuable research data.

9,600 Port Packages have been installed. From this point onward the annual number of installs will reduce to as few as ten (10), leaving close to 1,500 homes and apartments under the flight paths, overwhelmingly lower income people of colour, with no sound insulation.

The Third Runway opens on Nov 20th. The final cost is over $1.1B. Auditing begins immediately. However, just as the nation has gotten over any anxieties about flying, the Great Recession hits, extending the stalled rebound in airport operations from 2000.

2009 Reconstruction Begins

Almost the moment the Third Runway opens, the Port shuts down the center runway 16C for a complete reconstruction. After that, it begins a rebuild of the eastern runway 16L/34R. Both projects were not fully completed until October 2015.

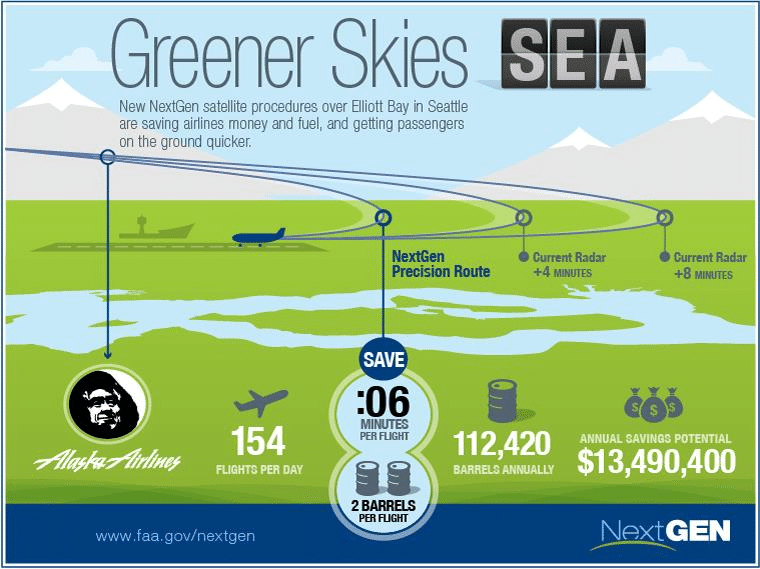

+2012 – Greener Skies

It passed almost unnoticed, but 2012 was the first time the Port of Seattle informs the surrounding governments that it will be updating its Master Plan. The FAA requires all major airports to maintain a master plan. And it requires those plans to be communicated to affected communities.

But the most transformative event in modern airports was the conversion to Greener Skies, which we’ve discussed in the NextGen For Dummies. The idea is to use electronic navigation to:

- Allow for planes to be closer together along all three axes (left, right, up, down, front, back)

- Concentrate flight paths over a much smaller area, thus making the areas impacted much, much smaller.

The system has been extremely successful in both regards.

+2014 Delta – courting new business

In 2014 Delta Airlines and Alaska ink an agreement making Sea-Tac the main hub for Delta Airlines. That began the real dramatic growth. Since then the big driver of air traffic has been towards Asia, both passenger and cargo.

+2015 The end of Reconstruction

With the completion of re-construction, first of the center runway 16C and then the eastern runway 16L/34R, Sea-Tac Airport reached its current configuration. Now there are at least two runways available at all times for parallel operations.

Plans to develop the southern end of the airport property as part of the SAMP are voted down by the Commission as being unnecessary and unduly expensive. All the Commissioners speak to the need to maintain an environmental buffer with the surrounding communities.

+2016 Virtual Runways

With NextGen, aircraft can be spaced closer together. But there is one remaining choke point in the sky: between the Tower and the TRACON.

Sea-Tac Airport shares the airspace with several other airports, including JBML and Boeing Field and King County International Airport KCIA. There is a delicate dance that air traffic controllers do in managing flights. The goal is to get everyone out of this virtual neighbourhood and into that wider space managed by the TRACON as fast as possible.

The FAA has a standard procedure for every flight, basically a list of instructions to direct the flight onto or off the airfield safely and efficiently within the framework of NextGen.

But the Tower also has the authority to create new customized routes within that 6-10 miles airspace they control and these are referred to as CATEX (category exclusions). So one CATEX might be that:

Q400 Turbo-Prop Aircraft departing north will immediately take a left turn over Burien/Seahurst over Puget Sound and then head towards their main heading to wherever their final destination may be.

This technique gives the Tower the flexilibility to clear the space more quickly, freeing up room for more departures.

Using a CATEX to creating new routes within Tower control is now referred to as a ‘Virtual Runway’. Every time the FAA issues another CATEX, the newly affected portion of the public complains. However, as the airport expands it will become a more common technique.

+2017 SAMP Wake up call

In 2017, the Port of Seatle unveils the first draft of the Sustainable Airport Master Plan, the official process necessary to move to the next level of capacity. The plan is broken into phases: Near Term Projects (NTP) and Long Term Projects (LTP).

2019 PSRC Vision 2050

As we saw in 1996, the PSRC is the key to Federal transportation funding. And the key to opening that funding is a demand study. The demand study is a legal requirement, but it is always rolled out as a marketing pitch. The Regional Aviation Baseline Study provides the legal basis for FAA approval.

+2022

After several delays, the comment period for the SAMP Near Term Projects will finally kick begin in autumn 2022. All SEPA and NEPA reviews appear on the front end of the process. The actual work product done by the consultant takes much longer and there is no mechanism during that time for the community to monitor their work or influence the process. They work closely with the airport, but not with the community.

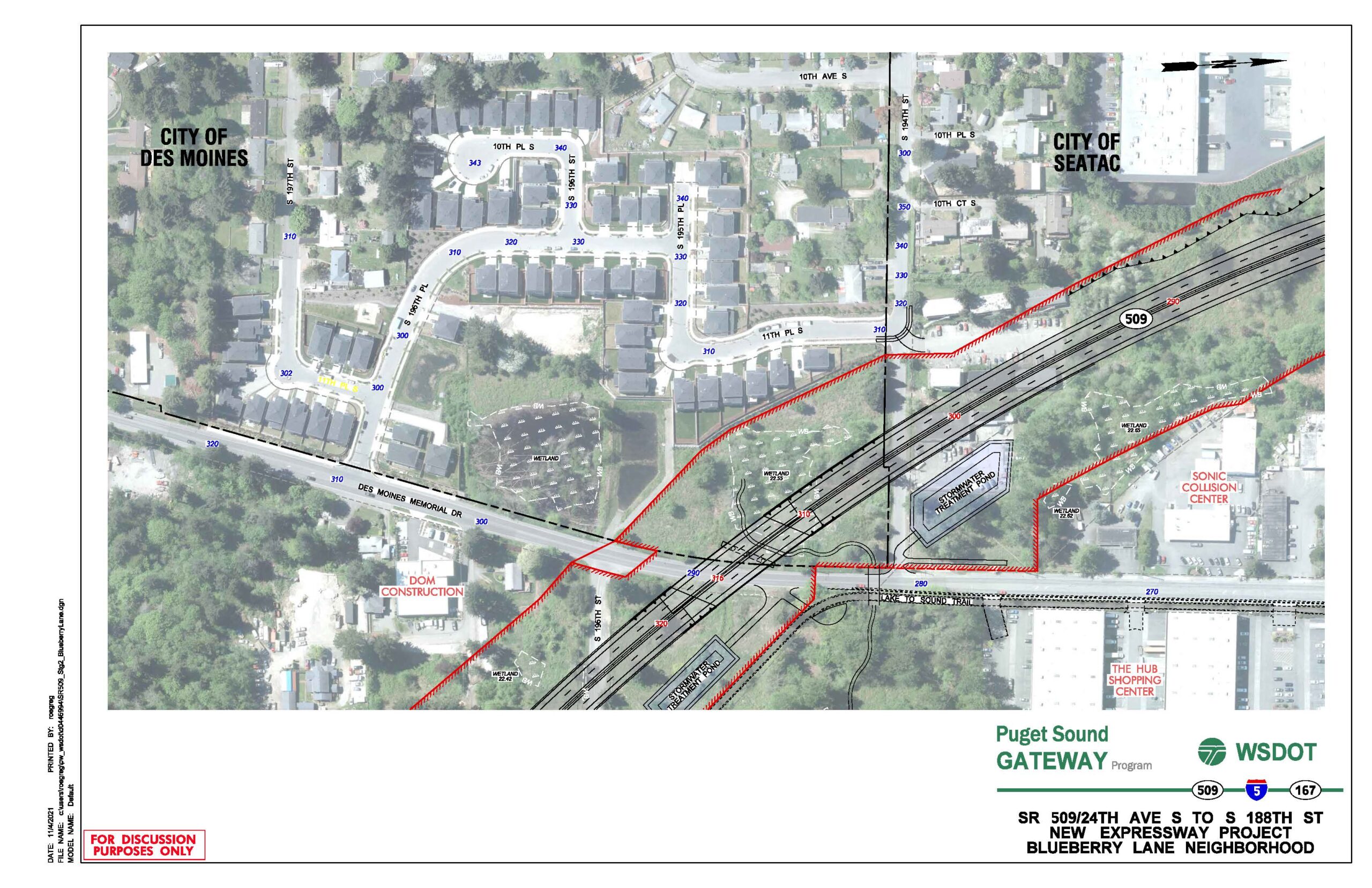

+2027 The Fourth Runway

In 2027, the Near Term Projects are expected to reach their conclusion, in tandem with the opening of SR-509 Stage II. 2027 will enable an increase in operations we’re calling The Fourth Runway because 2027 – 2034 will yield as big an increase in operations as the opening of the Third Runway in 2008.

For the first time in airport history, cargo will be able to use the same automation that seaports have enjoyed for many years and move at highway speed from the runway to I-5, SR-167 and the Kent Valley.

If you look at any major seaport, the whole point is to move cargo fast. You want to unload the cargo and get it out of the yard as quickly as possible and onto its final destination. To do that, seaports have also counted on a direct connection to the rail and freeway system.

For seaports, the choke point was always loading and unloading. They solved for that starting a decade ago just as all warehouses do: robots. It’s hard to express the increase in productivity. Ships that used to take weeks to unload and then return to sea now can get back out to sea in only a few days.

Currently, air freight has no such luxury at Sea-Tac Airport. Cargo loading and unloading is not fully automated and trucks have to navigate surface streets to get out to the main highways.

In 2027, SR-509 will open with a high speed exit directly off the airfield. Trucks will go directly onto 167 and I-5 or into the Kent Valley. The window between now (2022) and 2027 gives the airport the opportunity to build the automation to take full advantage of that new asset.

…and on to LTP….

The Long Term Projects are where the real money is. If demand is as expected. The Port will certainly want to revisit their 2015 decision not to develop the southern end of the property. Since no viable ‘second airport’ will be on the horizon, the cost (and profitability) of that land will make it a necessity.

Conclusions…

In our introduction, we asked what the Port got for the $1.1 billion dollar cost of the Third Runway. We would suggest two things:

- First, future capacity. Despite the 300% cost overruns, the Port has still been able to generate enough money over the past 20 years and has positioned itself as the single viable option for meeting both passenger and cargo needs of the region for the foreseeable future.

- And second, the Port was able to maintain a monopoly status. By building the Third Runway, and then taking a series of strategic steps, it was able to fend off any number of contenders. So now, regardless of how well they perform, Sea-Tac Airport is and will continue to be the only game in town.

The communities should also take a few important lessons from this:

300% cost overruns seem to be a habit. Going back to the original terminal, in 1949, paying three times the original price has been the rule rather than the exception. One might comment on management or politics or maybe even corruption. But one thing is for sure: the Port cannot seem to lose money. No matter how much projects cost, the Port always comes out ahead. So the lesson for the community should be: dream large. The Port can afford it.

Finally, while many of these events offered some form of community input, only one (the Third Runway) offered any substantial opportunity for mitigation and restitution. And yet, aside from some money for schools and some plumbing it would have had to pay for regardless, the communities got nothing.

The ‘key drivers’ of the airport growth are in this document:

1. Shift from GA/Taxis to Carriers.

2. Shift from radar to GPS (NextGen).

3. Courting new markets (Delta and Asian carriers)

4. Courting -tourism-.

5. Amazon and other cargo. (which is more in the future)

6. IAF and SAMP projects (which increase ground capacity.)

A -lot- of the growth of Sea-Tac has been due to the Port’s -marketing-, not intrinsic demand. The Port -courted- carriers to come here. A port is a port is a port. Seaports, airports all -compete- with one another for carriers. They wanted more carriers because that is where the money is.

Look at Item #1. All carrier flights have either a $4 or $8 passenger facilities charge per PASSENGER. So when you move from 50/50 mix of GA to carrier, although the total ops may be the same, the passenger explodes. And that means your revenue doubles. All those PFCs are money the Port can use for aviation-related purposes but NOT for community-related mitigations. So you go from under $300MM revenue in 2000 to $660MM in 2019.

The Port would push back and say that the carriers are actually -good- for the environment since each larger plane pollutes less per passenger.